Mastering Minority Interest

Nadia Lodroman | Oracle EPM Consultant | Integrity in Every Insight.

Listen to Tresora and Ledgeron's chatting about this blog post:

Handling Complex Ownership in Oracle FCCS

- Company B Ownership (Parent): 78%

- Minority Partner Ownership (NCI): 22%

- Consolidation Method: Subsidiary (Voting interest > 50%)

- Company B’s Investment in C: $100 USD

- Company C’s Equity (Paid-in Capital): $120 USD

- FCCS posts a calculated entry to the member FCCS_Minority Interest Income.

- On your Consolidated Income Statement, this appears as a deduction.

- Bottom Line: You see the full operational picture (Revenue/Expenses), but the final Net Income Attributable to Owners correctly reflects only your 78% share.

- The $100 Investment in Company C is eliminated (Credit).

- The $120 Paid-in Capital from Company C is eliminated (Debit).

- Calculation: $120 (Equity) * 22% = $26.4

- Result: FCCS creates a liability entry to FCCS_Minority Interest. This sits on the Consolidated Balance Sheet to show what the group "owes" the minority partner.

- Parent's Share: $120 (Equity) * 78% = $93.6$

- The Gap: The Parent paid $100 for a share worth $93.6.

- Result: The difference of $6.4 is automatically booked to Goodwill.

Turning financial complexity into operational clarity. Because in Finance, Integrity is Permanent.

General EPM Strategy FAQs

Why should a company use EPM Automate instead of custom scripting

EPM Automate allows for robust, bi-directional data orchestration between Oracle EPM and source ERPs (like NetSuite or Fusion) using native capabilities. It is highly scalable, easier to maintain during Oracle's monthly updates, and avoids the fragility of heavy custom coding.

Can Oracle Cloud EPM integrate with multiple different ERPs simultaneously?

Yes. Through strategic data pipeline architecture, Oracle EPM can ingest, consolidate, and even write-back finalized data to multiple disparate ERPs concurrently, acting as the single source of truth for the enterprise.

How does Oracle FCCS handle Minority Interest (NCI) and CTA?

While standard FCCS provides out-of-the-box functionality, complex global enterprises often require advanced configuration to isolate and calculate Minority Interest (NCI) and Cumulative Translation Adjustments (CTA) accurately at the top consolidated hierarchy without relying on manual journals.

Can you bypass the out-of-the-box Goodwill calculation in Oracle FCCS?

Yes. By utilizing advanced native configuration and custom consolidation rules, you can bypass standard Goodwill Input/Offset functionality to meet highly specific, non-standard acquisition accounting requirements.

How many daily transactions can Oracle ARCS process?

Oracle ARCS is built for enterprise scale. With proper architecture in the Transaction Matching engine, ARCS can easily process and auto-match hundreds of thousands of daily banking transactions, representing billions of dollars in value.

What is the difference between Transaction Matching and Reconciliation Compliance in ARCS?

Transaction Matching automates the high-volume, line-by-line matching of data (like daily bank feeds or ACH). Reconciliation Compliance is used to govern the period-end justification of broader balance sheet account balances.

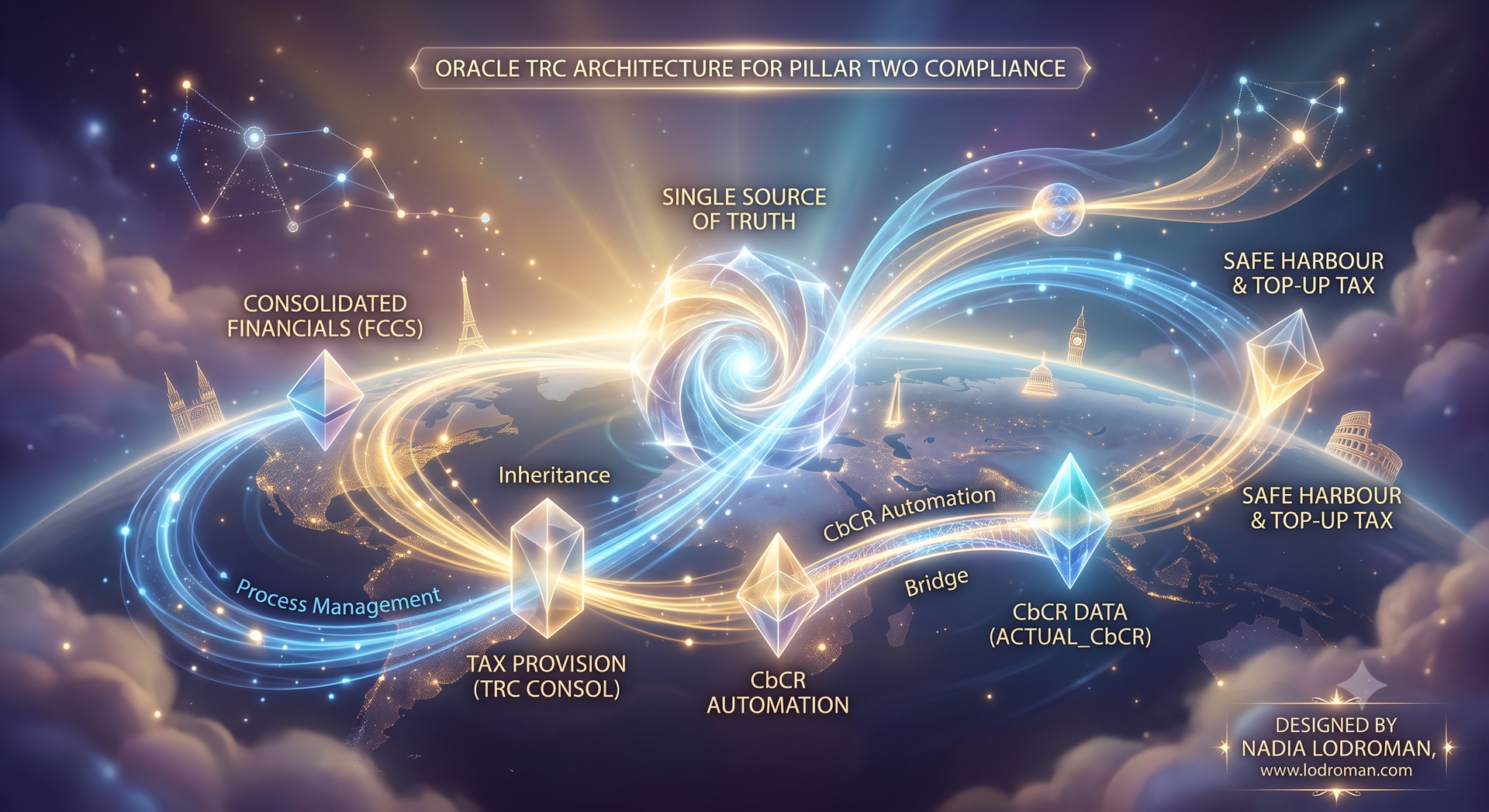

Does Oracle TRC handle Country-by-Country Reporting (CbCR)?

Yes. Oracle Tax Reporting Cloud (TRC) provides built-in frameworks to automate Country-by-Country Reporting, ensuring multinational organizations remain compliant with global BEPS (Base Erosion and Profit Shifting) regulations.

How does Oracle TRC integrate with FCCS?

TRC and FCCS share the same platform architecture, allowing for seamless data flow. Finalized pre-tax consolidated data from FCCS feeds directly into TRC for tax provisioning, ensuring perfect alignment between the finance and tax departments.

Still have a question?

All things Oracle EPM