Mastering Consolidations in Oracle FCCS: From Ownership to Equity Pickup

Nadia Lodroman | Oracle EPM Consultant | Integrity in Every Insight.

Listen to Tresora and Ledgeron's chatting about this blog post:

A Deep Dive into Oracle FCCS Consolidation and the Nuances of the Equity Method

- Subsidiary: Used when ownership confers control, typically over 50%. In this case, 100% of the subsidiary's assets, liabilities, and P&L are combined with the parent's. The portion not owned by the parent is calculated and backed out as Non-Controlling Interest (NCI).

- Proportional: Often applied to joint ventures where control is shared. The parent company includes its proportionate share of each of the subsidiary's financial line items. For example, with a 40% ownership stake, 40% of the subsidiary's assets, liabilities, and P&L are brought into the consolidation.

- Equity: Applied when the investor has significant influence but not control, typically with ownership between 20% and 50%. This method is treated differently from the others, as we will explore in detail later.

- Not Consolidated: For minor investments (usually under 20%), where the investment is typically held at its initial cost.

- Entity Input: This is the raw, standalone trial balance data for the child entity, either loaded from a source system or entered directly.

- Proportion: The system applies the relevant ownership percentage to the Entity Input data. For a Subsidiary, this will be 100%. For Proportional, it will be the ownership percentage (e.g., 40%). The result is stored in the Proportion member.

- Elimination: This crucial step prevents the overstatement of financials by removing intercompany transactions and balances. FCCS automatically identifies balances between a parent and child (or between two sister subsidiaries) and posts eliminating entries at the first common parent in the hierarchy. This ensures that, for example, an intercompany loan and its corresponding note payable net to zero in the consolidated view. These adjustments are stored in the Elimination member.

- Contribution: This is the final, netted result. It represents the sum of the Proportion and Elimination members. The total Contribution from all children, added to the parent's own data (Entity Consolidation), produces the final consolidated numbers for the group.

- The Equity Method: This is the accounting principle. It dictates that when you have significant influence (e.g., 30% ownership), you don't consolidate the investee's assets and liabilities line-by-line. Instead, you recognize your initial investment on your balance sheet as a single line item ("Investment in Associate"). Then, periodically, you adjust the value of that investment and recognize your share of the associate's profit or loss on your income statement.

- Equity Pickup (EPU): This is the process within FCCS for performing that periodic adjustment. When you enable the Equity Pickup feature in FCCS, it deploys dedicated rules and dimension members (EPU in the Data Source dimension) to automate this calculation.

- Trigger: The process is triggered for entities consolidated using the Equity Method.

- Calculation: The core EPU rule calculates the change in the subsidiary's total equity for the period (essentially, its net income less any dividends paid).

- Adjustment: The rule then "picks up" the parent's ownership share of that change. It posts this amount to two key places on the parent company's books:

- It debits (increases) the "Investment in Associate" account on the Balance Sheet.

- It credits (increases) the "Income from Equity Companies" account on the Income Statement.

Turning financial complexity into operational clarity. Because in Finance, Integrity is Permanent.

General EPM Strategy FAQs

Why should a company use EPM Automate instead of custom scripting

EPM Automate allows for robust, bi-directional data orchestration between Oracle EPM and source ERPs (like NetSuite or Fusion) using native capabilities. It is highly scalable, easier to maintain during Oracle's monthly updates, and avoids the fragility of heavy custom coding.

Can Oracle Cloud EPM integrate with multiple different ERPs simultaneously?

Yes. Through strategic data pipeline architecture, Oracle EPM can ingest, consolidate, and even write-back finalized data to multiple disparate ERPs concurrently, acting as the single source of truth for the enterprise.

How does Oracle FCCS handle Minority Interest (NCI) and CTA?

While standard FCCS provides out-of-the-box functionality, complex global enterprises often require advanced configuration to isolate and calculate Minority Interest (NCI) and Cumulative Translation Adjustments (CTA) accurately at the top consolidated hierarchy without relying on manual journals.

Can you bypass the out-of-the-box Goodwill calculation in Oracle FCCS?

Yes. By utilizing advanced native configuration and custom consolidation rules, you can bypass standard Goodwill Input/Offset functionality to meet highly specific, non-standard acquisition accounting requirements.

How many daily transactions can Oracle ARCS process?

Oracle ARCS is built for enterprise scale. With proper architecture in the Transaction Matching engine, ARCS can easily process and auto-match hundreds of thousands of daily banking transactions, representing billions of dollars in value.

What is the difference between Transaction Matching and Reconciliation Compliance in ARCS?

Transaction Matching automates the high-volume, line-by-line matching of data (like daily bank feeds or ACH). Reconciliation Compliance is used to govern the period-end justification of broader balance sheet account balances.

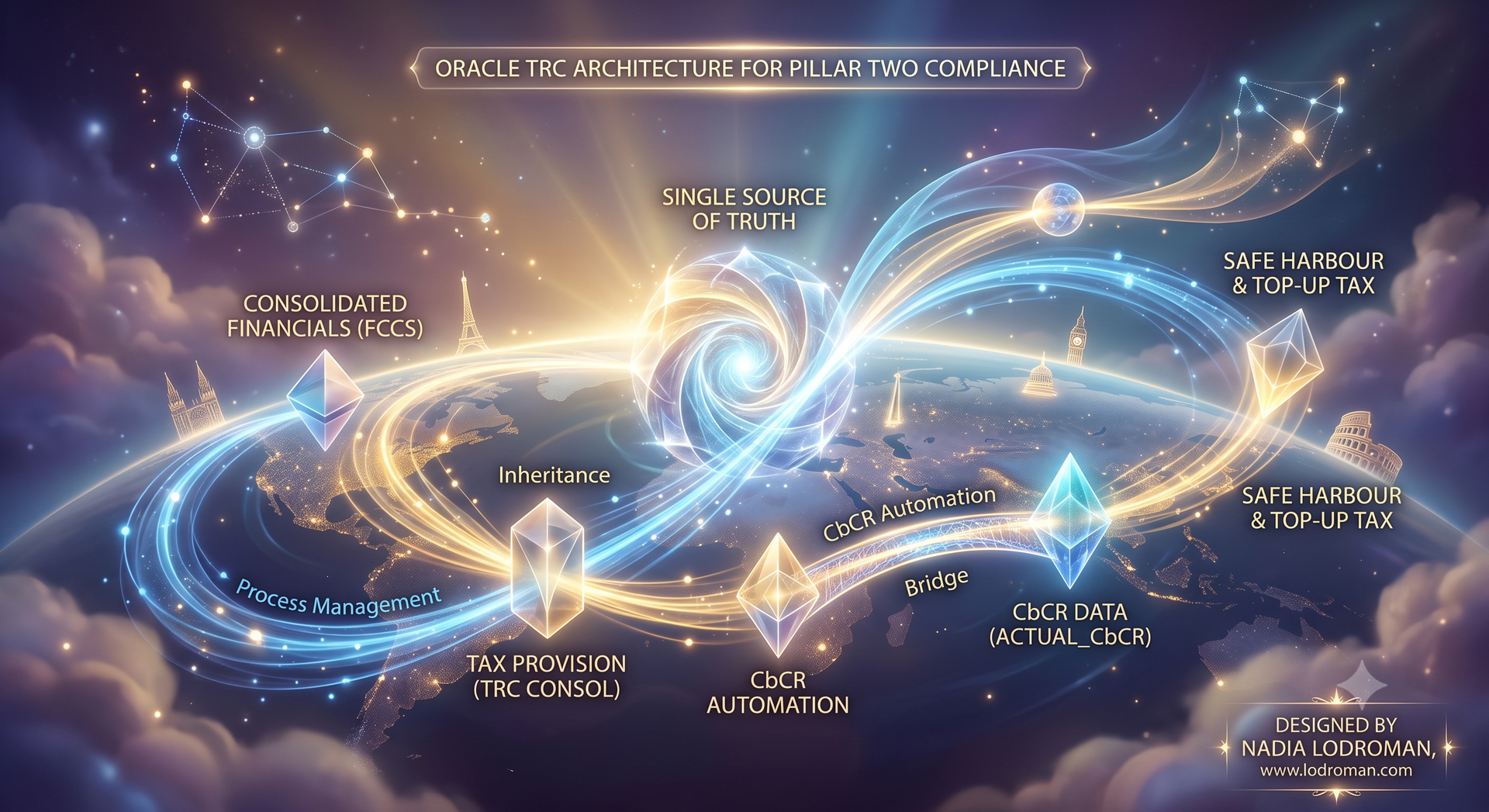

Does Oracle TRC handle Country-by-Country Reporting (CbCR)?

Yes. Oracle Tax Reporting Cloud (TRC) provides built-in frameworks to automate Country-by-Country Reporting, ensuring multinational organizations remain compliant with global BEPS (Base Erosion and Profit Shifting) regulations.

How does Oracle TRC integrate with FCCS?

TRC and FCCS share the same platform architecture, allowing for seamless data flow. Finalized pre-tax consolidated data from FCCS feeds directly into TRC for tax provisioning, ensuring perfect alignment between the finance and tax departments.

Still have a question?

All things Oracle EPM