Strategic Optimization of Oracle Tax Reporting

Nadia Lodroman | Oracle EPM Consultant | Integrity in Every Insight.

Listen to Tresora and Ledgeron's chatting about this blog post:

The "Silenced Mirror" Approach for Complex Global Hierarchies

In modern multinational finance organizations, the pressure to maintain perfect alignment between financial consolidation and tax reporting has never been higher. For many organizations, this results in a TRC Entity dimension that is a massive, complex mirror of the FCCS hierarchy. However, a significant technical challenge often emerges: while the hierarchy must be complete for consolidation and transparency, frequently only a small fraction (perhaps 20%) of these entities actually require a Corporate Tax (CT) provision calculation. The remaining "stateless" or non-calculating entities can create unnecessary noise in the tax engine.

The most effective way to resolve this is through the "Silenced Mirror" Strategy. This methodology allows organizations to preserve the integrity of their FCCS-aligned hierarchy while surgically disabling the tax engine where it isn't needed.

The Case for the Mirrored Hierarchy

The decision to keep the TRC hierarchy in sync with FCCS is driven by the fundamental need for seamless reconciliation.

- Apples-to-Apples Reconciliation: By mirroring the FCCS structure, tax teams can perform a direct reconciliation of Net Income Before Tax (NIBT) at any level of the organization, ensuring the starting point for tax calculations is identical to the financial close.

- Clean Data Governance: Maintaining a single governance process for account mapping ensures that any localization changes, secondary ledger adjustments, or chart of account transitions are reflected consistently across all reporting modules.

- Entity-Level Accuracy: A synchronized hierarchy allows for corrections—such as purchase price accounting (PPA) adjustments or the reclassification of entries incorrectly booked in a single entity—to be handled at the base entity level rather than as opaque consolidation adjustments.

Silencing the Engine via Jurisdiction Management

Rather than segregating the hierarchy—which creates a massive maintenance burden—performance is optimized by leveraging the Jurisdiction dimension.

- Stateless Jurisdiction Assignment: All entities that do not require a CT provision should be assigned to a specific "Stateless" or "No Jurisdiction" member in the Jurisdiction dimension.

- Computational Efficiency: TRC’s tax engine is rule-driven. By ensuring that no tax rates, tax automation rules, or regional attributes are defined for this "Stateless" member, the engine effectively ignores these entities during the automated calculation process.

- Functional Currency Governance: This setup also provides a clear framework for managing functional currency changes. If an entity's economic environment shifts, it can be migrated to a new entity within the same logical hierarchy, ensuring that Currency Translation Adjustments (CTA) remain accurate during consolidation.

Enhancing User Experience through Valid Intersections

To prevent the 80% of stateless entities from cluttering the user interface, administrators should utilize Valid Intersections.

- Artifact Suppression: By creating a rule that renders tax-specific Data Source members (like TRCS_Tax) invalid for stateless entities, you effectively hide tax forms and dashboards from users who don't need them.

Database Optimization: This approach prevents the system from creating empty data blocks for non-calculating entities, which keeps the application "small" and ensures that the consolidation engine remains fast and responsive.

Fulfilling Global Transparency Mandates

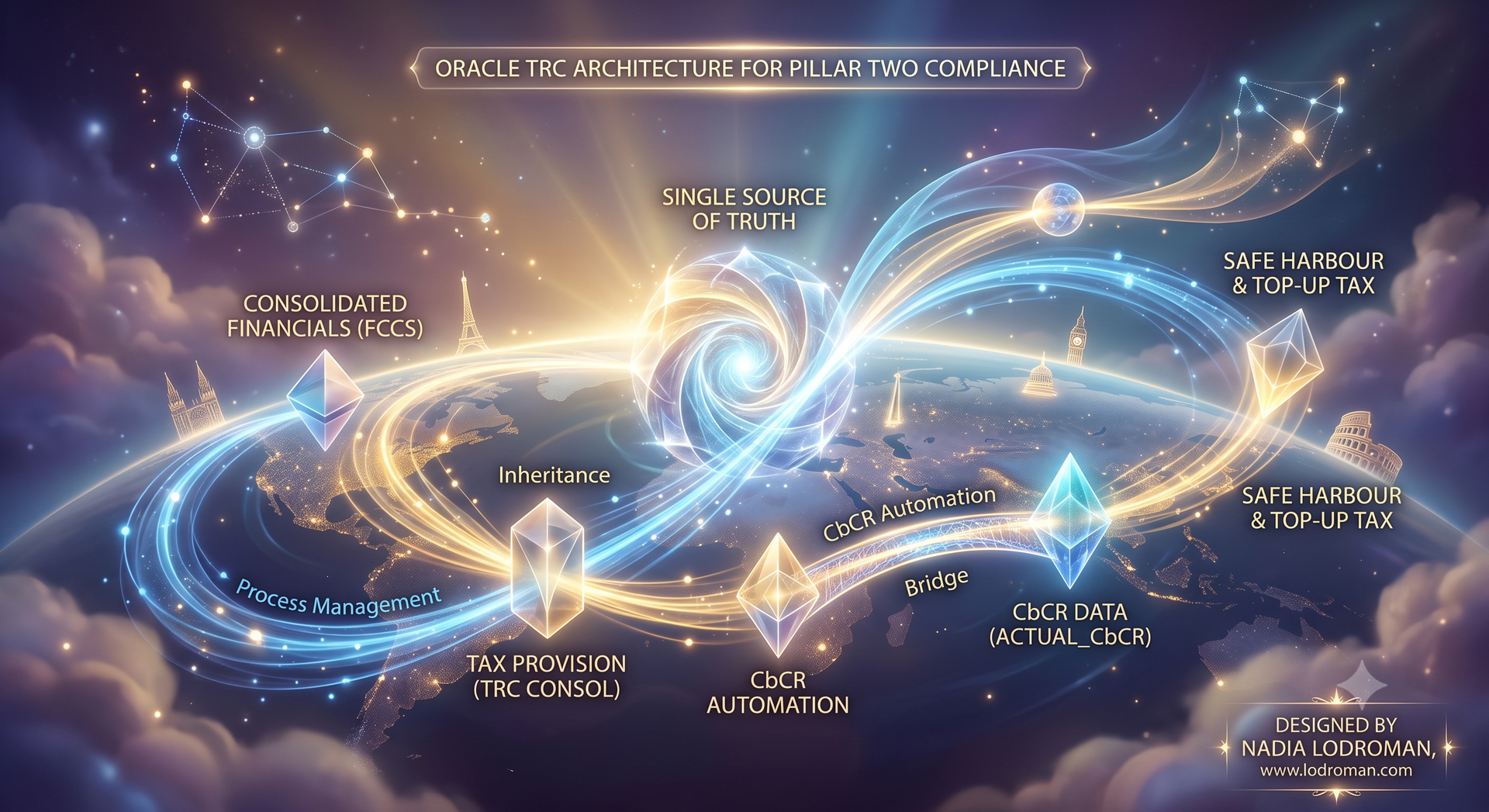

The "Silenced Mirror" strategy is not just about performance; it is a requirement for modern regulatory compliance, specifically for Country-by-Country Reporting (CbCR) and Pillar Two.

- OECD CbC Compliance: OECD guidelines explicitly require that entities not resident in any tax jurisdiction be reported under a "Stateless" category. This assignment in TRC allows for the accurate generation of CbC XML files and jurisdictional summaries.

- Pillar Two Blending Models: The GloBE rules for Pillar Two require jurisdictional blending. By keeping stateless entities within the main hierarchy, their revenues, profits, and taxes (or lack thereof) are correctly aggregated into the blending models used to calculate jurisdictional ETRs and Top-up Taxes.

Final Conclusion

By embracing Oracle's recommended approach of a mirrored hierarchy supported by Jurisdiction assignments and Valid Intersections, organizations can achieve a high-performance environment that satisfies both the local tax team and global regulators. This strategy eliminates the need for fragmented hierarchies, simplifies metadata maintenance, and provides a future-proof foundation for the evolving landscape of global tax transparency.

For more insights into Oracle EPM best practices, visit us at www.lodroman.com.

Turning financial complexity into operational clarity. Because in Finance, Integrity is Permanent.

General EPM Strategy FAQs

Why should a company use EPM Automate instead of custom scripting

EPM Automate allows for robust, bi-directional data orchestration between Oracle EPM and source ERPs (like NetSuite or Fusion) using native capabilities. It is highly scalable, easier to maintain during Oracle's monthly updates, and avoids the fragility of heavy custom coding.

Can Oracle Cloud EPM integrate with multiple different ERPs simultaneously?

Yes. Through strategic data pipeline architecture, Oracle EPM can ingest, consolidate, and even write-back finalized data to multiple disparate ERPs concurrently, acting as the single source of truth for the enterprise.

How does Oracle FCCS handle Minority Interest (NCI) and CTA?

While standard FCCS provides out-of-the-box functionality, complex global enterprises often require advanced configuration to isolate and calculate Minority Interest (NCI) and Cumulative Translation Adjustments (CTA) accurately at the top consolidated hierarchy without relying on manual journals.

Can you bypass the out-of-the-box Goodwill calculation in Oracle FCCS?

Yes. By utilizing advanced native configuration and custom consolidation rules, you can bypass standard Goodwill Input/Offset functionality to meet highly specific, non-standard acquisition accounting requirements.

How many daily transactions can Oracle ARCS process?

Oracle ARCS is built for enterprise scale. With proper architecture in the Transaction Matching engine, ARCS can easily process and auto-match hundreds of thousands of daily banking transactions, representing billions of dollars in value.

What is the difference between Transaction Matching and Reconciliation Compliance in ARCS?

Transaction Matching automates the high-volume, line-by-line matching of data (like daily bank feeds or ACH). Reconciliation Compliance is used to govern the period-end justification of broader balance sheet account balances.

Does Oracle TRC handle Country-by-Country Reporting (CbCR)?

Yes. Oracle Tax Reporting Cloud (TRC) provides built-in frameworks to automate Country-by-Country Reporting, ensuring multinational organizations remain compliant with global BEPS (Base Erosion and Profit Shifting) regulations.

How does Oracle TRC integrate with FCCS?

TRC and FCCS share the same platform architecture, allowing for seamless data flow. Finalized pre-tax consolidated data from FCCS feeds directly into TRC for tax provisioning, ensuring perfect alignment between the finance and tax departments.

Still have a question?

All things Oracle EPM