Leveraging CbCR as the Foundation for GloBE Compliance

Nadia Lodroman | Oracle EPM Consultant | Integrity in Every Insight.

Listen to Tresora and Ledgeron's chatting about this blog post:

Strategy First: Using CbCR as your Pillar Two Shield.

In the transition to the OECD’s Pillar Two (Global Minimum Tax), many organizations feel they are standing at the base of a mountain of data. The sheer volume of data points required for a full GloBE calculation - spanning deferred tax recaptures, intercompany dividends, and substance-based exclusions - is enough to overwhelm even the most robust tax departments.

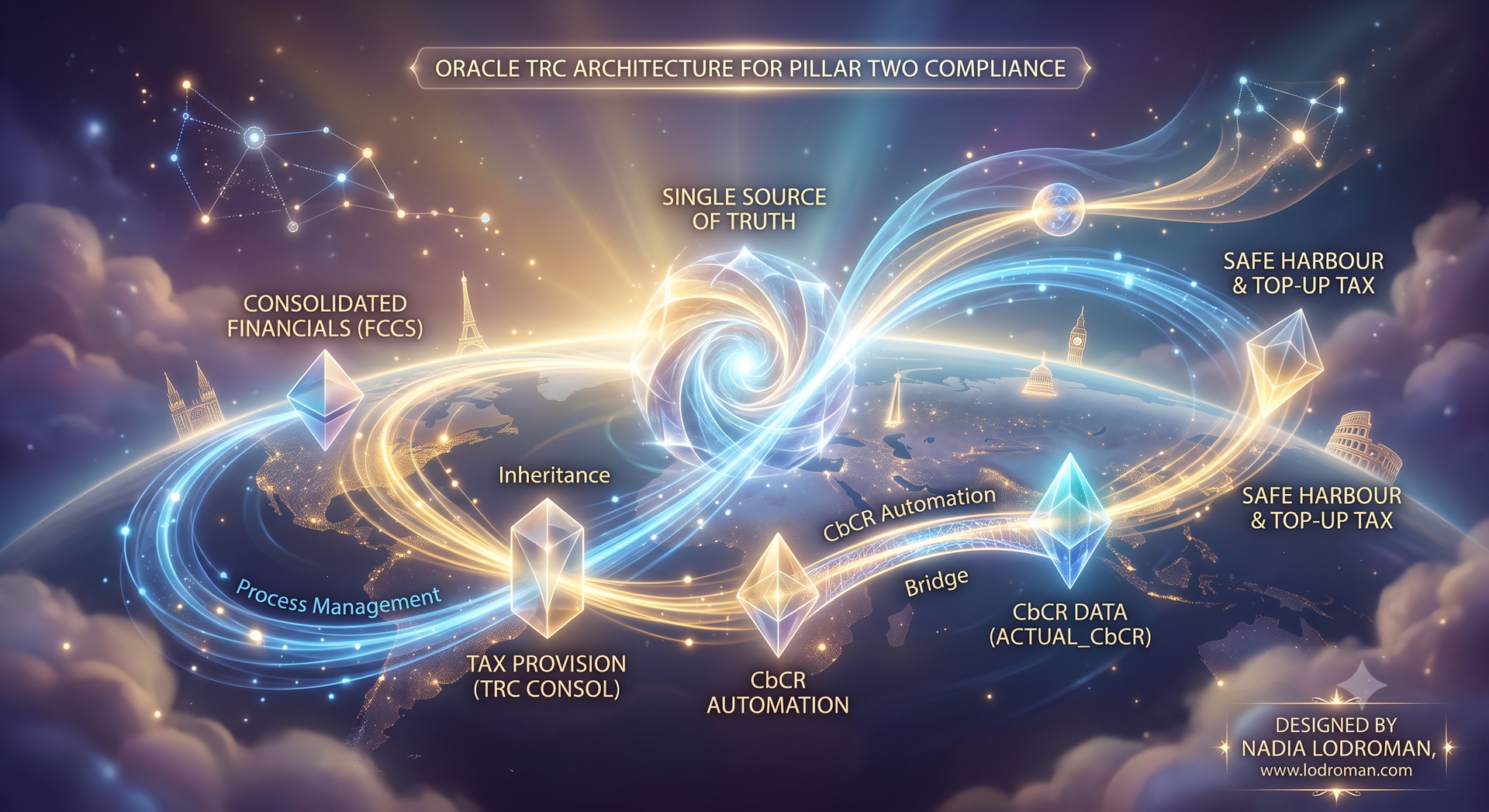

However, the architecture of Oracle Tax Reporting (TRCS) offers a strategic path forward. By design, Oracle has positioned Country-by-Country Reporting (CbCR) as the structural gateway to Pillar Two. This choice was deliberate: it reflects the OECD’s own reliance on CbCR as the primary risk-assessment tool. By mastering your CbCR data today, you can effectively "shield" your organization from the grueling complexity of full GloBE calculations for years to come.

1. The Strategic Shield: Transitional Safe Harbours

The most immediate value of this CbCR-first approach is the ability to leverage the Transitional CbCR Safe Harbour. For the transition years (now extended into 2026 and 2027 by recent OECD guidance), Oracle TRCS uses your automated CbCR Table 1 data to perform three critical tests:

- The De Minimis Test: Identifying jurisdictions with less than €10M in revenue and €1M in profit.

- The Simplified ETR Test: Checking if the jurisdictional ETR (Simplified Covered Taxes / Profit Before Tax) meets the transition threshold (rising from 15% to 17% by 2026/2027).

- The Routine Profits Test: Determining if the profit is lower than the Substance-Based Income Exclusion (SBIE).

A "Green" result on any of these tests means the Top-up Tax is deemed zero. You effectively "shield" that jurisdiction from the full GloBE calculation, saving hundreds of hours of manual data entry and a significantly reduced audit burden.

2. The Architectural Integrity: Mapped from the "Financial Close"

A common challenge in tax reporting is data fragmentation. Oracle solves this through CbCR Automation. The system is designed to "pull" data from the Consol cube (the source of your financial provision) directly into the CbCR cube.

In my work with clients, I emphasize the absolute necessity of "Qualified Financial Statements" (QFS). For a Safe Harbour to be valid, the data must be auditable and derived from the same audited numbers used in your FCCS (Financial Close) consolidation. Oracle’s automation rules allow us to map FCCS accounts - like Total Revenue and PBT - directly to the CbCR Table 1 columns. This creates an airtight audit trail that links your financial close to your Pillar Two strategy. If your CbCR automation is not robust, your Pillar Two strategy is built on sand.

3. The "Once Out, Always Out" Risk

Establishing true expertise means understanding the high stakes of configuration. The OECD applies a strict "Once Out, Always Out" rule to the Transitional Safe Harbour. If an organization fails to elect or qualify for the Safe Harbour in a jurisdiction in Year 1, they are disqualified from using it in all subsequent transition years.

One needs to ensure that the initial TRCS configuration is not just a "technical set-up" but a strategic audit. We look for the "data traps" - such as incorrectly mapped intercompany revenue or non-covered taxes - that could accidentally trigger a "Fail" on a safe harbour test and force an organization into years of unnecessary complexity.

Key Technical Insights for the Board:

- Automation: Table 1 and Table 2 should be 90% automated from the financial close to ensure QFS compliance.

- Auditability: Every "Safe Harbour" election should be backed by a drill-down report in TRCS showing the underlying source accounts.

- Future-Proofing: The 2026/2027 extension of the CbCR Safe Harbour makes this the most high-ROI area of your EPM roadmap today.

Is Your CbCR Data Safe-Harbour Ready?

Pillar Two compliance is a journey, not a switch. If you are uncertain whether your current Country-by-Country Reporting process is robust enough to trigger the Transitional Safe Harbours, your organization is carrying unnecessary risk.

I specialize in the architecture and oversight required to turn technical requirements into strategic stability.

Let’s have a conversation about auditing your CbCR data pipeline. Ensure that integrity in your data creates stability in your global tax strategy.

Turning financial complexity into operational clarity. Because in Finance, Integrity is Permanent.

General EPM Strategy FAQs

Why should a company use EPM Automate instead of custom scripting

EPM Automate allows for robust, bi-directional data orchestration between Oracle EPM and source ERPs (like NetSuite or Fusion) using native capabilities. It is highly scalable, easier to maintain during Oracle's monthly updates, and avoids the fragility of heavy custom coding.

Can Oracle Cloud EPM integrate with multiple different ERPs simultaneously?

Yes. Through strategic data pipeline architecture, Oracle EPM can ingest, consolidate, and even write-back finalized data to multiple disparate ERPs concurrently, acting as the single source of truth for the enterprise.

How does Oracle FCCS handle Minority Interest (NCI) and CTA?

While standard FCCS provides out-of-the-box functionality, complex global enterprises often require advanced configuration to isolate and calculate Minority Interest (NCI) and Cumulative Translation Adjustments (CTA) accurately at the top consolidated hierarchy without relying on manual journals.

Can you bypass the out-of-the-box Goodwill calculation in Oracle FCCS?

Yes. By utilizing advanced native configuration and custom consolidation rules, you can bypass standard Goodwill Input/Offset functionality to meet highly specific, non-standard acquisition accounting requirements.

How many daily transactions can Oracle ARCS process?

Oracle ARCS is built for enterprise scale. With proper architecture in the Transaction Matching engine, ARCS can easily process and auto-match hundreds of thousands of daily banking transactions, representing billions of dollars in value.

What is the difference between Transaction Matching and Reconciliation Compliance in ARCS?

Transaction Matching automates the high-volume, line-by-line matching of data (like daily bank feeds or ACH). Reconciliation Compliance is used to govern the period-end justification of broader balance sheet account balances.

Does Oracle TRC handle Country-by-Country Reporting (CbCR)?

Yes. Oracle Tax Reporting Cloud (TRC) provides built-in frameworks to automate Country-by-Country Reporting, ensuring multinational organizations remain compliant with global BEPS (Base Erosion and Profit Shifting) regulations.

How does Oracle TRC integrate with FCCS?

TRC and FCCS share the same platform architecture, allowing for seamless data flow. Finalized pre-tax consolidated data from FCCS feeds directly into TRC for tax provisioning, ensuring perfect alignment between the finance and tax departments.

Still have a question?

All things Oracle EPM